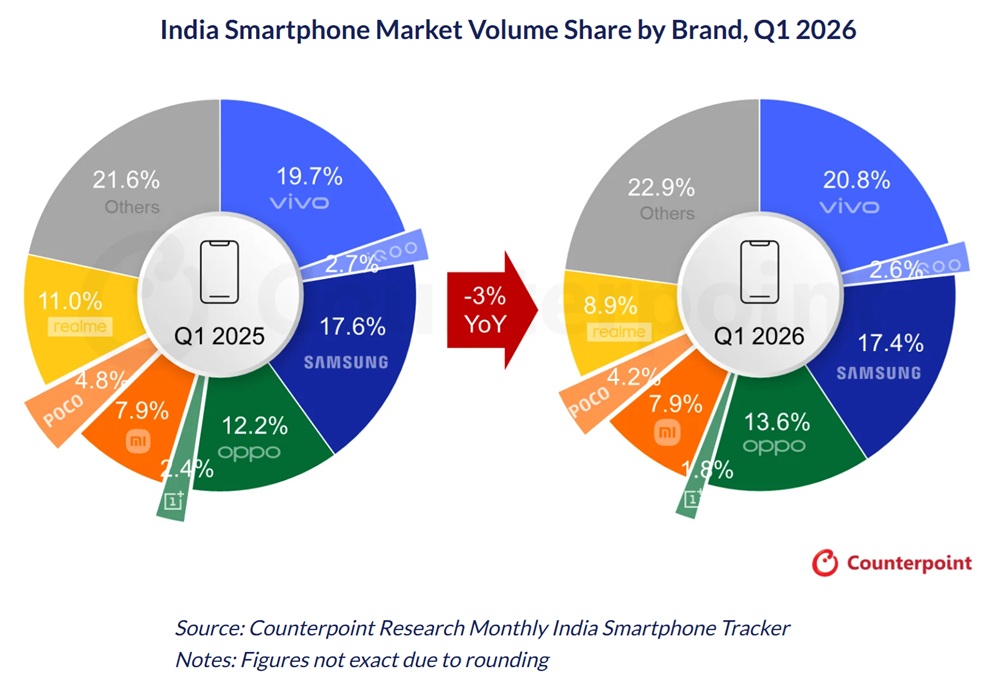

India’s smartphone market declined 3% year-on-year in Q1 2026, marking its weakest quarter in six years, according to Counterpoint Research’s Monthly India Smartphone Tracker. The decline came despite higher launch activity, as rising component costs, OEM price increases, and weak consumer demand reduced retail conversions across channels.

Senior Analyst Prachir Singh said the market is facing a clear affordability squeeze driven by memory-led inflation and currency pressure. He noted that average price increases have exceeded ₹1,500, with the sub-₹15,000 segment impacted the most due to high price sensitivity.

He added that rising energy costs and geopolitical tensions are further straining household budgets, leading consumers to prioritize essentials. As he stated, “upgrade cycles are stretching,” and recovery in the mass market is expected to remain gradual.

India smartphone shipments drop in Q1 2026

India’s smartphone shipments fell 3% YoY in Q1 2026 due to a combination of supply-side and demand-side pressures.

Key factors included:

- Sharp rise in memory and component costs

- OEM-led price increases across key models

- Weak demand in entry-level segments

- Currency fluctuations increasing BOM (Bill of Materials) costs

- Higher household and energy expenses reducing discretionary spending

Nearly one-third of model launches were advanced to Q1 to offset rising component costs and reduce further BOM inflation, particularly due to memory pricing and currency fluctuations.

Over 80 smartphone models saw an average price hike of 15% in Q1. A further 15%–20% price increase is expected in Q2, driven by sustained cost pressure. Memory prices are projected to increase by 80%–85% sequentially, further impacting affordability.

Brand rankings in Q1 2026

vivo leads market with 21% share

vivo (excluding iQOO) led the Indian smartphone market with a 21% share. Growth was driven by an expanded portfolio, higher number of launches, strong traction in the mid-premium segment led by the V series, and disciplined channel execution.

Samsung holds second position

Samsung ranked second, supported by strong demand for A-series models including A07, A36, and A56. The brand also saw early response to the Galaxy S26 series, with record pre-bookings led by the Ultra variant. Samsung recorded its highest shipment contribution from the ₹15,000–₹20,000 segment, supported by a balanced portfolio across price tiers.

OPPO becomes fastest-growing top-five brand

OPPO (excluding OnePlus) held third position with a 14% share and grew 8% YoY, becoming the fastest-growing brand among the top five. Growth was driven by strong performance in the budget segment through A and K series and steady traction in the Reno mid-premium segment. Portfolio expansion also supported momentum.

Xiaomi (including POCO) ranks fourth

Xiaomi remained fourth, with strong growth in the ₹10,000–₹20,000 segment supported by improved dual-channel execution and a sharper focus on hero models, leading to better retail traction and returns.

realme strong in online segment

realme saw strong traction in the ₹10,000–₹20,000 segment in online channels and ranked among the top two brands in this category. Models such as P3 Lite and Narzo 80 Lite contributed to demand.

Apple reaches 9% share

Apple’s shipment share reached 9% in Q1 2026, driven by strong momentum of the iPhone 17 series. Growth was supported by long-term EMI schemes and exchange offers. Apple is better positioned to manage memory cost pressures due to its premium portfolio and supply chain efficiency.

Fastest-growing brands and emerging trends

Nothing leads growth with 47% YoY

Nothing (including CMF) was the fastest-growing brand in Q1 2026 with 47% YoY growth. It has been the fastest-growing brand in eight of the last nine quarters.

Growth was driven by accelerated offline expansion, the launch of its first exclusive retail store in India, and strong early traction for the Phone (4a) series. The series resonated with younger, design-focused consumers due to its design language, software experience, and camera performance.

Flipkart confirmed that the Phone (4a) series became the best-selling smartphone on Day 1 in the ₹30,000+ segment, indicating strong demand in the category. Expansion into offline retail further strengthened its omnichannel presence in India.

Google fastest-growing in premium segment

Google was the fastest-growing brand in the premium segment (>₹45,000), growing 39% YoY. Growth was driven by AI-focused features, the Pixel Upgrade Program, and increased visibility through major sporting events such as the ICC World Cup and IPL.

OnePlus leads affordable premium segment

OnePlus emerged as the leading brand in the ₹30,000–₹45,000 segment on Amazon, supported by consistent demand for the Nord series. The new Nord 6 series is expected to support further growth.

Chipset market trends

MediaTek led the India smartphone chipset market with a 49% share, while Qualcomm led the premium Android segment (>₹30,000) with over 50% share.

Outlook

Research Director Tarun Pathak said the India smartphone market is expected to remain under pressure in the near term, with Q2 2026 likely to see a double-digit decline. For the full year, the market is projected to decline by 10% YoY.

He noted that sustained memory price inflation, which has increased nearly 4x over the past three quarters, continues to impact affordability and extend replacement cycles. In this environment, brands are expected to remain disciplined, focusing on premium-led growth, tighter portfolio execution, and improved channel efficiency.

Overall, while the premium segment is expected to remain relatively stable, weak mass-market demand is likely to result in a gradual and uneven recovery.