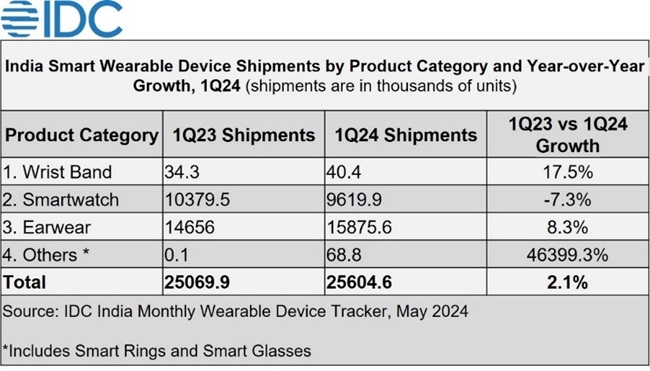

According to IDC’s India Monthly Wearable Device Tracker, India’s wearable device market grew by 2.1% year-over-year (YoY) to 25.6 million units in 1Q24.

This growth was limited by high inventory from the festive quarters in the second half of 2023. The average selling price (ASP) for wearables dropped by 17.8%, from $22.62 to $18.59, the lowest on record.

Key Highlights of 1Q24: India’s Wearable Device Market

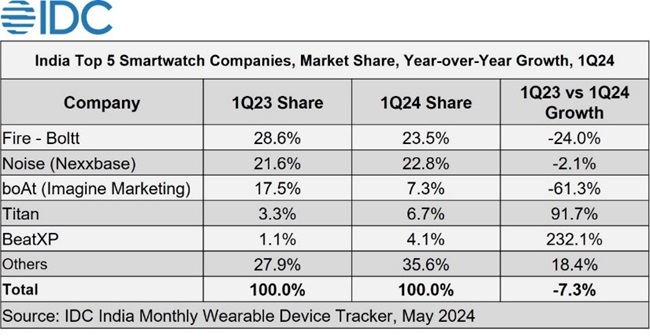

Smartwatch Market

- Decline in Shipments: Smartwatch shipments fell for the first time since 4Q18, by 7.3% YoY to 9.6 million units.

- Market Share Drop: The share of smartwatches within wearables decreased to 37.6% from 41.4% in 1Q23.

- Average Selling Price: ASP for smartwatches declined from $29.24 to $20.65, due to sales events and discounts.

- Advanced Smartwatches: The share of advanced smartwatches rose from 2.0% to 3.2%.

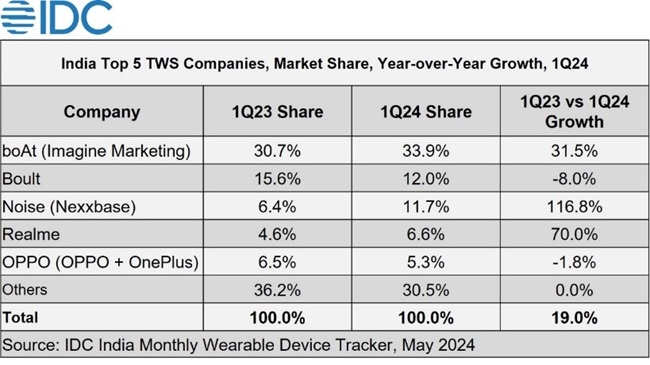

Earwear Market

- Growth in Shipments: Earwear shipments increased by 8.3% YoY to 15.9 million units.

- TWS Segment: The Truly Wireless Stereo (TWS) segment’s share grew from 63.8% to 70.1%, marking a 19% YoY increase.

- Other Earwear: Shipments of other earwear types (tethered and over-ear) declined by 10.6%.

- Average Selling Price: ASP for earwear fell by 7.3% to $16.62.

Market Share and Vendor Performance

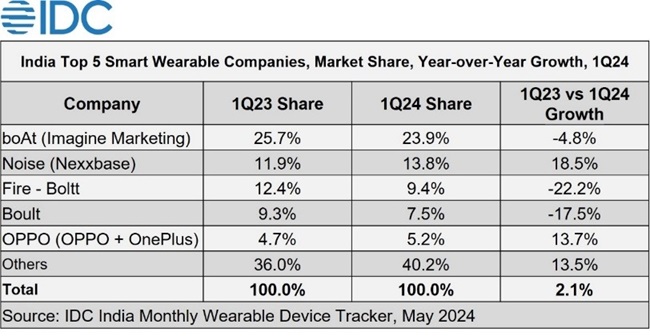

- Top Vendors: The top five vendors (BoAt, Noise, Fire-Bolt, Boult, and Oppo) maintained their positions, though their collective market share decreased from 63.9% to 59.9%.

- Smartwatch Category: High inventory levels led to a decline in shipments for the top three vendors, but Titan and BeatXP saw their shipments double and triple, respectively.

- Earwear Category: All top five vendors, except Boult, increased their shipments.

Retail and Distribution Trends

- Offline Channel Growth: The share of offline channels increased to 37.9% from 26.1% in 1Q23.

- Online Channel Decline: Online shipments fell by 14.1% YoY, marking the second consecutive quarter of decline.

- Retail Partnerships: Vendors are expanding retail presence through partnerships with national and regional retail chains and bundling wearables with products like smartphones and laptops.

Anand Priya Singh, Market Analyst for IDC India, notes that retail partnerships and product bundling may revive growth in the festive sales period later this year.

Emerging Categories

Smart Rings: 64,000 smart rings were shipped in 1Q24, with an ASP of $173.06. Ultrahuman led this market with a 43.9% share, followed by Pi Ring at 40.1% and Aabo at 8.4%.

Market Outlook

According to Vikas Sharma, Senior Market Analyst for IDC India, the smartwatch market in India is beginning to show signs of a slowdown due to limited innovation and difficulty in encouraging customers to upgrade.

IDC expects a low double-digit decline in smartwatch shipments for 2024. However, earwear shipments are projected to grow by mid-single digits, driven by advancements in AI and features like active noise cancellation.