India’s traditional PC market—including desktops, notebooks, and workstations—achieved its strongest year ever in 2025, shipping 15.9 million units, up 10.2% YoY, according to IDC’s Worldwide Quarterly Personal Computing Device Tracker.

This is the first time annual shipments surpassed 15 million units, exceeding the pandemic-driven peaks of FY2021 and FY2022. The market showed strong momentum in the final quarter, with 4Q25 shipments reaching 4.1 million units, reflecting 18.5% YoY growth.

Category Performance Highlights

- Notebooks: Remained the largest category, growing 12.4% YoY in 2025, with 23.9% YoY growth in 4Q25.

- Desktops: Recorded moderate gains, rising 3.6% YoY in 2025 and 6.2% YoY in 4Q25.

- Workstations: Fastest-growing segment, expanding 24.2% YoY in 2025 and 18.7% YoY in 4Q25, driven by “professional and high-performance computing” demand.

Premium notebooks (above US$1,000) grew 8.2% YoY, supported by rising demand for high-performance devices. AI-enabled notebooks surged 129.3% YoY, with basic AI models representing 86.6% of total AI notebook shipments. GenAI notebooks gained traction among consumers, led by Apple’s MacBook portfolio, which captured 70.9% share in this category.

Commercial and Consumer Segment Performance

- Commercial PCs: Shipped 8.6 million units, with enterprise growth at 20.9% YoY and SMB growth at 8.2% YoY. Strong enterprise demand and partial fulfillment of the ELCOT deal boosted 4Q25 shipments to 2.6 million units, driven by “robust momentum.”

- Consumer PCs: Shipped 7.3 million units, growing 3.6% YoY. Online demand during festive sales and aggressive channel stocking supported performance, although 4Q25 saw a slight 2.6% YoY decline due to delayed supplies.

- eTail channel: Expanded rapidly, 12% YoY in 2025 and 5.2% YoY in 4Q25, driven by “wider geographic reach” and competitive discounts.

According to Bharath Shenoy, Research Manager, IDC India & South Asia, “PC shipments in the consumer segment grew YoY for the second consecutive year,” driven by media, content creation, and gaming. He added that “AI PCs and vendor investments in AI capabilities” are expected to further accelerate demand, although processor shortages in late 2025 caused temporary supply constraints.

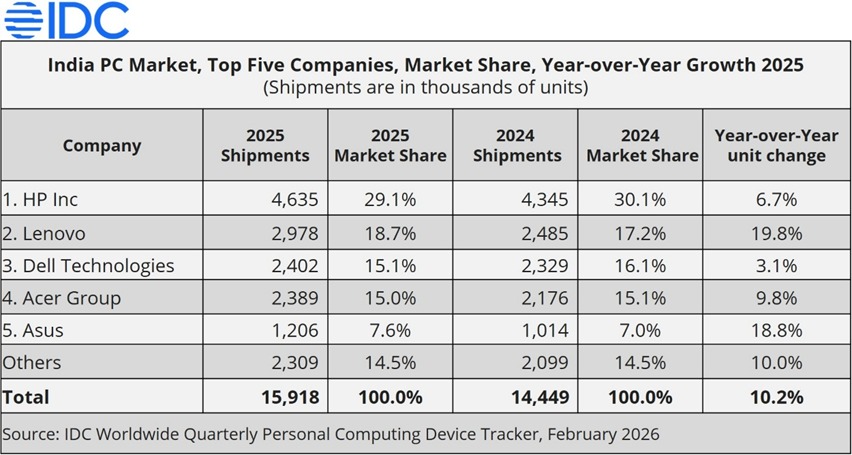

Top Vendor Performance

- HP Inc. (29.1% share) – Led overall market. Commercial segment grew 18.7% YoY, while consumer declined 9.4% YoY due to weaker OmniBook traction. In 4Q25: 34.3% commercial share, 24.8% consumer share.

- Lenovo (18.7% share) – Delivered balanced growth across segments. Commercial share 19.9%, consumer share 17.3%. In 4Q25: 20.2% consumer share, 16.9% commercial share.

- Dell Technologies (15.1% share) – Strong commercial growth of 18.3% YoY supported by AMD-powered portfolio and enterprise demand. Overall shipments declined 27.7% YoY due to inventory clearance and supply issues. In 4Q25: 24% commercial share, 9.2% consumer share.

- Acer Group (15.0% share) – Commercial grew 5.8% YoY, consumer expanded 15.7% YoY driven by entry-level notebooks and “aggressive eTail push.” In 4Q25: 17.7% commercial share, 10.2% consumer share.

- ASUS (7.6% share) – Consumer grew 12% YoY through offline expansion via LFR channels. Commercial surged 98.3% YoY via eTail and offline growth. In 4Q25: 12.1% consumer share, 1.9% commercial share.

Market Outlook: Component Costs Could Challenge Growth

Despite record 2025 performance, rising prices for DDR RAM, GPUs, and processors may affect affordability in 2026.

According to Navkendar Singh, Associate VP, IDC India, South Asia & ANZ, “PC prices rose over 10% YoY in 2025 and may increase another 15–20%,” especially impacting SMBs and government segments. Processor shortages may also limit entry-level PC availability, potentially shifting demand toward tablets and smartphones.