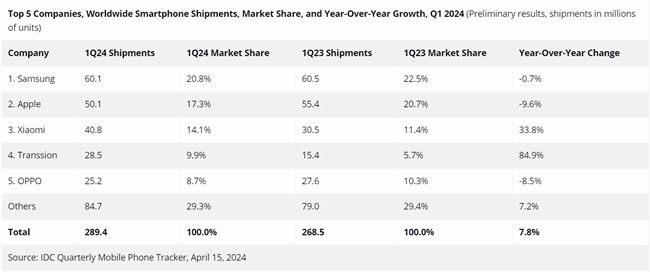

Global smartphone shipments saw a rise of 7.8% year over year, totaling 289.4 million units in the first quarter of 2024 (1Q24), according to the IDC Worldwide Quarterly Mobile Phone Tracker.

Despite ongoing economic challenges in various markets, this marks the third consecutive quarter of shipment growth, signaling a robust recovery.

Top 5 Companies in Q1 2024

- Samsung: Leading the pack with 60.1 million units shipped, holding a market share of 20.8%. Although there’s a slight decrease in shipments compared to Q1 2023, Samsung gained in market share.

- Apple: Securing the second position, Apple shipped 50.1 million units, commanding a 17.3% market share. However, there’s a decline in shipments by 9.6% compared to the same quarter last year.

- Xiaomi: Occupying the third spot, Xiaomi shipped 40.8 million units, claiming a 14.1% market share. Impressively, this reflects a substantial increase in shipments by 33.8% from Q1 2023.

- Transsion: Ranking fourth, Transsion shipped 28.5 million units, capturing a 9.9% market share. Notably, there’s a significant surge in shipments by 84.9% from Q1 2023.

- OPPO: Holding the fifth position, OPPO shipped 25.2 million units, with an 8.7% market share. However, there’s a decline in shipments by 8.5% from Q1 2023.

- Others: Collectively shipped 84.7 million units, constituting 29.3% of the market share in Q1 2024.

Market Recovery and Forecast

Ryan Reith, IDC’s group vice president, highlights the ongoing smartphone recovery, particularly among leading brands like Samsung, which reclaimed the top spot in Q1 2024.

While Apple and Samsung are poised to dominate the high-end market, the resurgence of HUAWEI in China and significant progress from Xiaomi, Transsion, OPPO/OnePlus, and vivo may prompt them to seek new avenues for growth.

Reith predicts that as the recovery progresses, major players will strengthen their positions, while smaller brands may face challenges establishing themselves in the market.

Key Trends and Insights

Nabila Popal, research director at IDC’s Worldwide Tracker team, emphasizes two significant trends: the rise in device value and average selling prices (ASPs), driven by consumer preference for longer-lasting, premium devices, and a shifting power dynamic among the top 5 companies.

This evolution is expected to continue as market players adapt their strategies in a post-recovery landscape. Popal underscores the persistence of this evolution as market players navigate the challenges and opportunities of a recovering market.

Commenting on the market dynamics, Nabila Popal, Research Director with IDC’s Worldwide Tracker team, remarked,

The smartphone market has navigated through the challenges of the past two years, emerging stronger and transformed. Xiaomi is rebounding vigorously from significant declines seen previously, and Transsion is solidifying its position in the Top 5 with robust expansion in global markets. However, despite experiencing negative growth in the first quarter, Samsung appears to be in a more favorable position compared to recent quarters, while the top two players faced similar challenges.