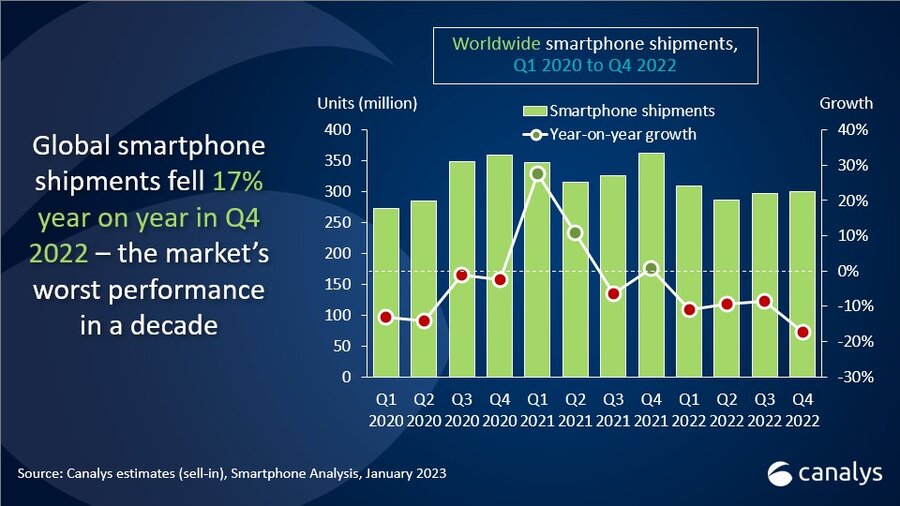

In the last quarter of 2022, the number of smartphones shipped globally decreased by 17% compared to the same period the previous year. The total number of smartphones shipped in 2022 also decreased by 11% to less than 1.2 billion, as per a report by Canalys, indicating a difficult year for all smartphone manufacturers. As per previous reports by Canalys, Indian smartphone shipments fell 6% YoY in Q3 2022.

Global smartphone market in Q4 2022

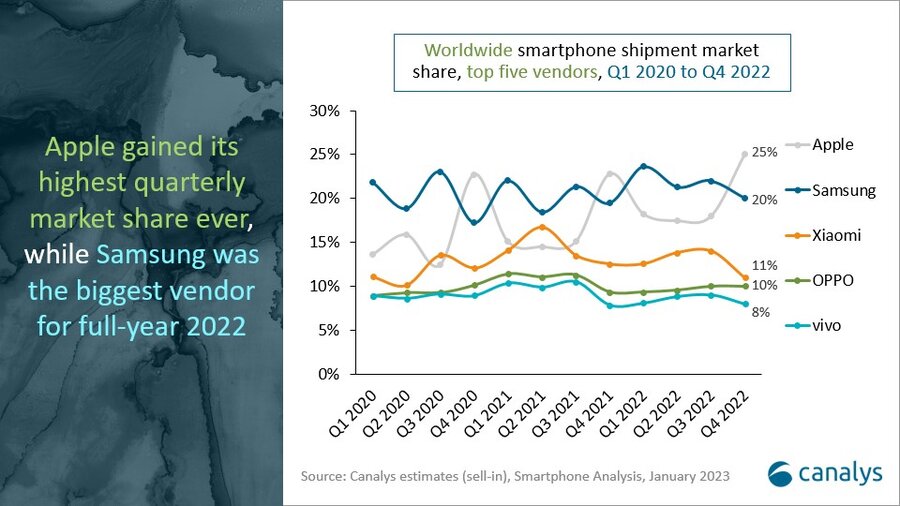

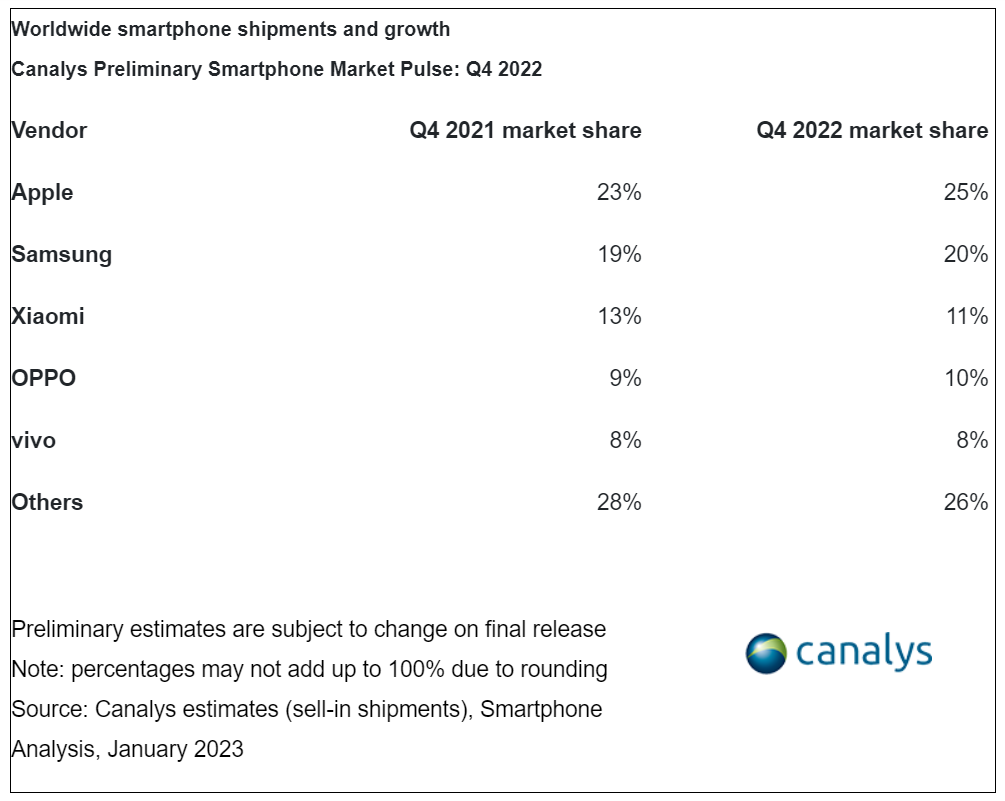

In the last quarter of 2022, Apple regained the top spot in the smartphone market with a 25% market share, the highest it has ever achieved. Despite facing declining demand and production problems in Zhengzhou, Samsung came in second place with a 20% market share.

However, it was still the largest vendor for the entire year. Xiaomi held on to the third spot, but its market share dropped to 11% due to difficulties in India. OPPO and vivo rounded out the top five, with 10% and 8% market shares respectively.

Smartphone market in 2023

According to a report by Canalys, smartphone vendors will be cautious in 2023 and focus on profitability and maintaining their market share. They will also be cutting costs to adapt to the current market conditions. Building strong relationships with their channel partners will be important to protect market shares, as difficult conditions can cause tension in negotiations. Canalys predicts that the smartphone market will see flat or only marginal growth in 2023 and conditions are expected to remain tough.

Factors such as inflation, interest rate hikes, economic slowdowns and a struggling labor market will limit the market’s potential, particularly in markets like Western Europe and North America. However, some regions such as Southeast Asia are expected to see economic recovery and growth in the second half of 2023, driven by an increase in tourism in China.

Commenting on the report, Canalys Research Analyst Runar Bjørhovde, said,

Smartphone vendors have struggled in a difficult macroeconomic environment throughout 2022. Q4 marks the worst annual and Q4 performance in a decade. The channel is highly cautious with taking on new inventory, contributing to low shipments in Q4. Backed by strong promotional incentives from vendors and channels, the holiday sales season helped reduce inventory levels. While low-to-mid-range demand fell fast in previous quarters, high-end demand began to show weakness in Q4. The market’s performance in Q4 2022 stands in stark contrast to Q4 2021, which saw surging demand and easing supply issues.