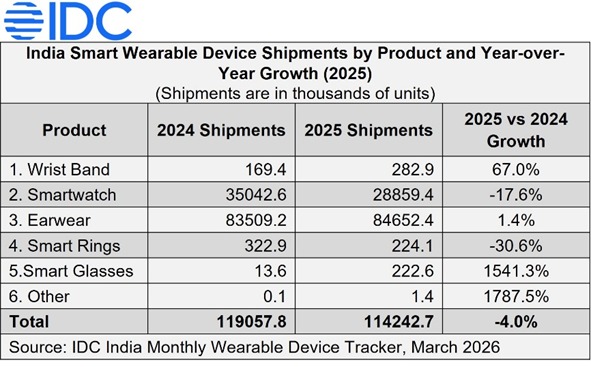

India’s wearable device market declined 4.0% year-over-year (YoY) in 2025, reaching 114.2 million units, marking its second consecutive annual decline, according to the India Monthly Wearable Device Tracker from International Data Corporation.

The downturn was primarily driven by a 17.6% YoY drop in smartwatch shipments. Despite softer shipment volumes, average selling prices (ASPs) increased 1.8% YoY to US$20.3, reflecting gradual premiumization and easing price erosion across wearable categories.

Smartwatch Shipments Continue to Decline

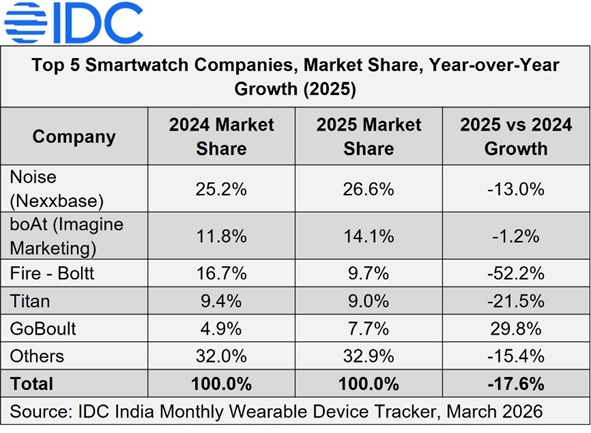

Smartwatch shipments declined 17.6% YoY in 2025, contributing significantly to the overall wearables market contraction.

Key data points include:

- Category market share: Declined to 25.3% in 2025, compared with 29.4% in 2024

- Smartwatch ASP: Increased 11.7% YoY, rising from US$23.8 in 2024 to US$26.5 in 2025

- Advanced smartwatch shipments: Declined 8.7% YoY

- Advanced smartwatch market share: Increased slightly from 2.9% in 2024 to 3.2% in 2025

IDC noted that vendors are shifting toward “better product differentiation” and “more sustainable pricing strategies” as the market matures.

Earwear Category Shows Modest Growth

The earwear category grew 1.4% YoY, reaching 84.7 million units in 2025. Despite shipment growth in certain segments, earwear ASP declined 1.1% YoY to US$17.5, reflecting intense competition in the mass-market TWS segment and aggressive online promotions.

Truly Wireless Stereo (TWS) devices remained the dominant category with a 70.2% share, although shipment volumes remained flat due to market maturity and longer replacement cycles.

Within earwear categories:

- Neckband shipments declined 10.2% YoY

- Over-the-ear headphones recorded the fastest growth, increasing 65.4% YoY to 7.4 million units

Vendor Performance

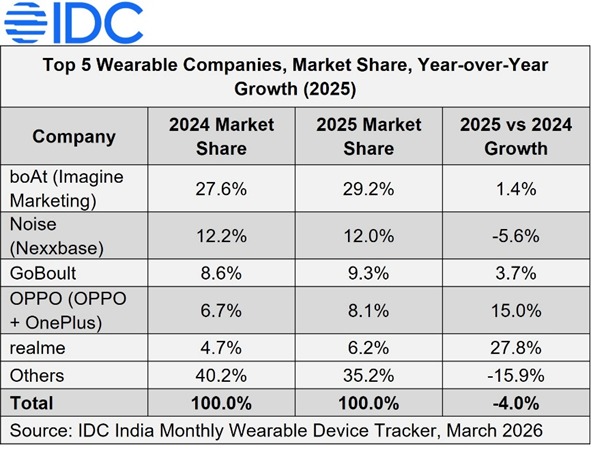

In the overall wearables market, boAt (Imagine Marketing) strengthened its leadership position in 2025, increasing its market share from 27.6% in 2024 to 29.2% in 2025. The brand maintained strong shipment volumes across TWS, tethered audio, and over-the-ear headphones.

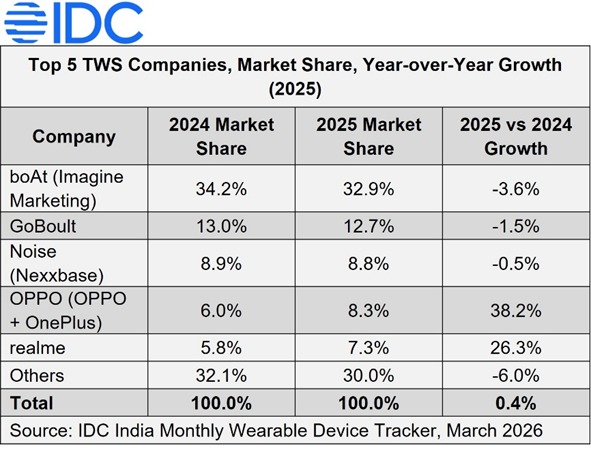

In the TWS segment, smartphone-led brands expanded their presence:

- Nothing (including CMF) recorded the highest growth at 91.5% YoY

- OPPO (including OnePlus) grew 38.2% YoY

The over-the-ear headphone segment also recorded strong growth, led by:

- boAt

- Samsung (JBL)

- Zebronics

Among emerging vendors:

- GoBoult recorded 698.3% YoY growth

- Noise (Nexxbase) recorded 276.5% YoY growth

In the smartwatch category:

- Noise led the market with 26.6% share

- boAt ranked second with 14.1% share

- Fire-Boltt ranked third with 9.7% share

- GoBoult ranked fifth with 29.8% YoY growth

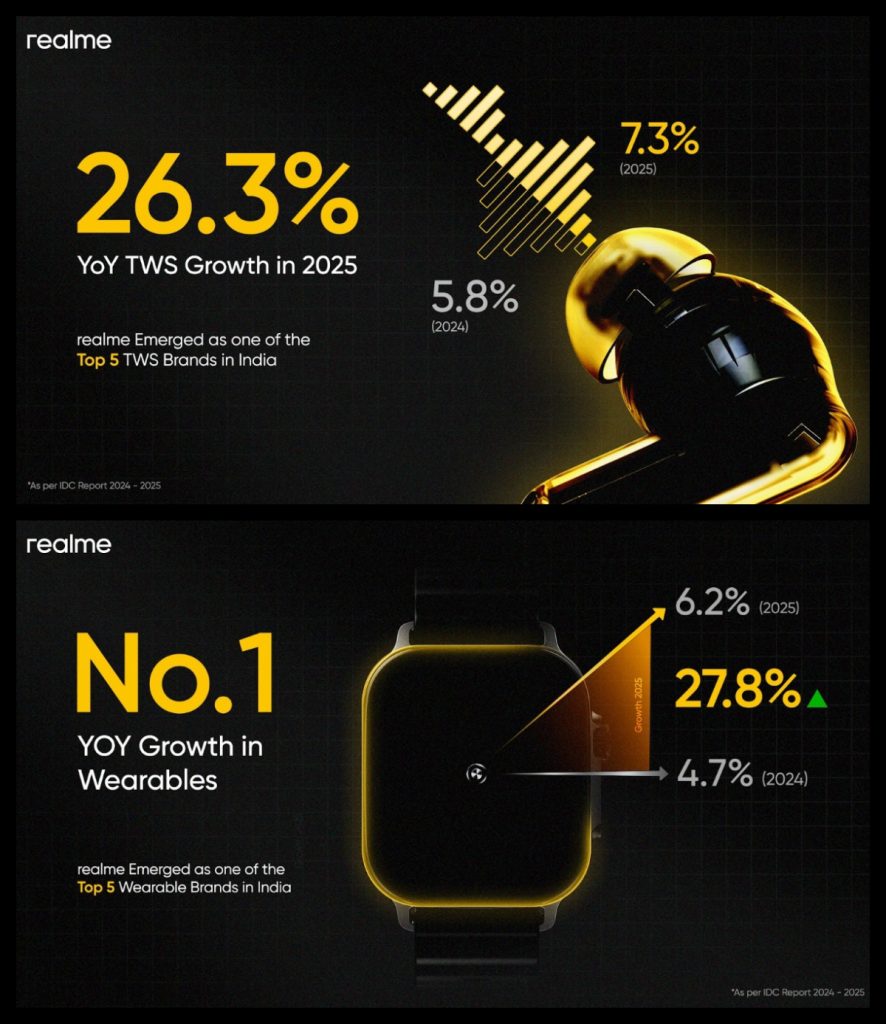

realme Records 27.8% Wearables Growth in 2025

Despite the overall market contraction, realme emerged as one of the top five wearable brands in India in 2025, according to International Data Corporation.

- 27.8% YoY growth in the overall wearables market compared to 2024, securing a 6.2% market share

- No. 5 position in the TWS segment, with 26.3% YoY growth and a 7.3% market share

Since 2025, realme has expanded its “Make in India” initiative by starting local manufacturing of its AIoT portfolio through a partnership with Optiemus Electronics Ltd..

Devices produced under this initiative include:

- realme Buds Air 8

- realme Buds Clip

- realme smartwatches

The partnership aims to produce 5 million AIoT devices annually, while creating over 2,000 jobs and strengthening India’s domestic electronics supply chain.

Offline Channel Gains Share

In 2025, the offline retail channel expanded its presence, growing 3.1% YoY and increasing its market share from 37.8% in 2024 to 40.7% in 2025. Meanwhile, the online channel declined 8.4% YoY. The online contraction was mainly driven by a 22.7% YoY drop in smartwatch shipments, while earwear shipments online declined 3.2% YoY.

In contrast, offline earwear shipments grew 9.4% YoY, supported by stronger retail demand. However, offline smartwatch shipments declined 10.5% YoY.

Emerging Wearable Categories

Emerging wearable categories also gained traction in 2025, driven by new product launches and evolving use cases.

Smart Glasses

Smart glasses recorded the fastest growth among wearable categories, with shipments surging 1,541.3% YoY.

Leading vendors included:

- Lenskart — 36.2% share

- Meta — 28.4% share

- Fire-Boltt — 17.1% share

The category’s ASP increased 152.4% YoY to US$112.6, supported by AI and imaging upgrades.

Smart Wristbands

Smart wristbands recorded a revival in 2025, growing 67.0% YoY to 0.3 million units.

- Samsung led the category with 59.0% share

- Pebble (SRK Powertech) ranked second with 14.2% share

Additional momentum came from WHOOP and Amazfit (Zepp), particularly with screenless band designs.

Smart Rings

Smart ring shipments declined 30.6% YoY in 2025.

- Ultrahuman led with 30.4% share

- Gabit ranked second with 18.3% share

The category’s ASP declined 8.7% YoY to US$159.7 as vendors including boAt, Aabo, and Fittr expanded product availability.

Smartwatch Market Outlook for 2026

Following a challenging 2025, the smartwatch market is expected to undergo a “reset” in 2026, with shipments projected to decline in the mid-single digits as the market shifts focus from volume expansion to higher-value devices and ecosystem integration.

According to Anand Priya Singh, market analyst for Smart Wearable Devices at IDC India, smartwatches are evolving beyond basic tracking, with “AI-led analytics,” “advanced sensors,” and “predictive health insights” shaping the next phase of the category.

Earwear Market Outlook for 2026

The earwear market is expected to grow in the low single digits in 2026 as the category matures and replacement cycles lengthen.

Vikas Sharma, Senior Market Analyst for Smart Wearable Devices at IDC India, noted that vendors are focusing on “AI-led real-time audio,” “personalized spatial sound,” and “ergonomic open-ear designs” to support higher ASPs.

He added that “strengthening offline reach” and addressing “increasingly sophisticated counterfeits in physical retail” will remain key priorities as the market stabilizes.